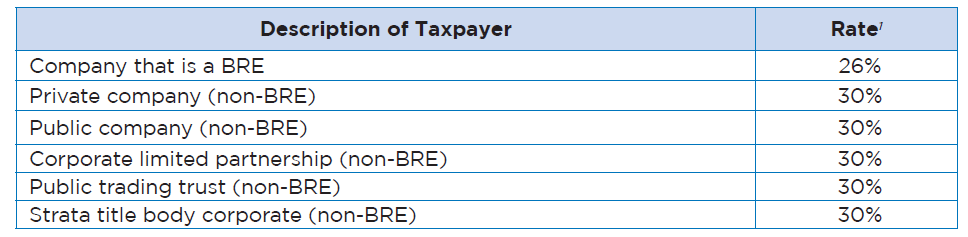

Company Rates of Tax – 2020/21

维州经营成本援助计划补助 • 解疑答惑

30/10/2021

专业人士的商业服务

23/12/2022

General Company Tax Rate

1 The rates in this table do not apply to Retirement Savings Account Providers, Life Insurance Companies, Pooled Development Funds, credit unions or non-profit companies.

Non-profit Company Tax Rates (other than BREs)

Non-profit BRE Company Tax Rates

Key Super Rates and Thresholds – 2020/21

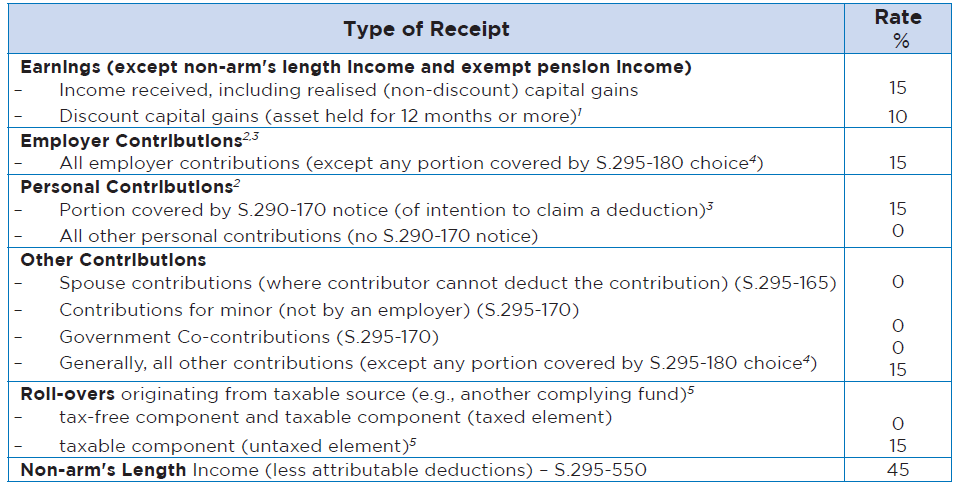

Complying Superannuation Fund Rates of Tax

Concessional Contributions – General Cap Concessional contributions include employer contributions (including contributions made under a salary sacrifice arrangement) and personal contributions claimed as a tax deduction.

1 From 2018/19, individuals with a total superannuation balance of less than $500,000 can make additional concessional contributions if they have unused cap amounts. Unused carried forward amounts expire after five years.

2 From 1 July 2021, the concessional contributions cap will be $27,500 as a result of indexation.

Non-concessional Contributions (‘NCCs’) – General Cap Non-concessionalNCCs include personal contributions for which taxpayers do not claim a tax deduction1.

Total Superannuation Balance on 30 June 2020 was greater than or equal to the general transfer balance cap of $1.6 million.

2 From 1 July 2021, the annual NCCs cap will be $110,000 as a result of indexation.

CGT Cap Amount CGT

An individual may elect for certain contributions made in connection with applying the CGT small business 15-year or retirement exemptions to count towards their lifetime CGT cap rather than their non-concessional contributions cap.

Government Co-contribution

General Transfer Balance Cap

The general transfer balance cap is used for various purposes, including to determine:

u the total capital amount that can be transferred into the retirement (pension) phase; and u eligibility for making non-concessional contributions.

1 From 1 July 2021, the general transfer balance cap will be $1.7 million as a result of indexation

Lump Sum Superannuation Benefits – Low Rate Cap Amount

The application of the low rate threshold for superannuation lump sum payments is capped.

1 From 1 July 2021, the low rate cap amount will be $225,000 as a result of indexation.

Superannuation Guarantee Rate

Employers who provide less than a prescribed level of superannuation support (the ‘charge percentage’) for their eligible employees will be liable to pay a superannuation guarantee charge based on the shortfall.

Disclaimer

This content is intended for general information in summary form on tax and legal matters at the time of first publication and is not intended to provide, and should not be relied upon in place of appropriate professional advice. Please consult your tax, legal and accounting advisors before acting or relying on any content provided.

References

https://www.ato.gov.au/rates/changes-to-company-tax-rates/